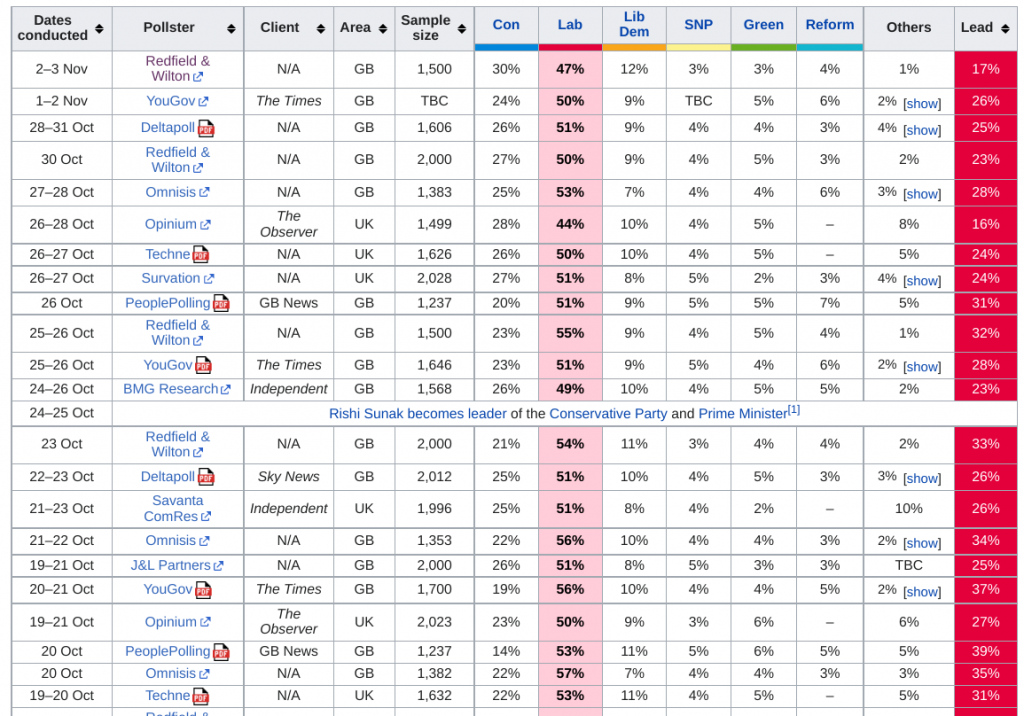

Sunak does appear to be helping a CON recovery in the polls – politicalbetting.com

Sunak does appear to be helping a CON recovery in the polls – politicalbetting.com

Sunak does appear to be helping a CON recovery in the polls – politicalbetting.com

0

This discussion has been closed.

Sunak does appear to be helping a CON recovery in the polls – politicalbetting.com

Comments

Heard it here first.

Fact is, The average Tory poll has to be around 27% an abysmal honeymoon bounce considering a previous leader and budget bounced it down there.

This problem is as bad as it is due entirely to talentless clueless incompetents the Tory’s put in charge of mangling it. There’s no magic bullet, it’s true, though here’s my list of things that will reduce the problem for sure,

1. For starters, The incompetents managing it don’t understand the problem they are dealing with - it’s as simple of that - we know this as fact as they talk about 70% or more are economic migrants, bogus asylum seekers. Back in the real world do you really believe Undocumented economic migrants deliver themselves into the hands of Home Office officials as soon as they reach UK soil? Hence, 4% processing comes from setting up for 70%+ economic migrants, not genuine asylum claims. According the governments own figures, the majority of asylum claims are found to be legitimate Almost two-thirds (64%) of asylum claims end in a grant of protection. Of those rejected that went on to appeal, 48% were successfully overturned. They are clearly tackling the backlog with the wrong mindset and wrong prioritising.

2. Secondly, on basis you now realise how many are genuine asylum claims bogged down in your two year backlog, Set up a Department for International Development (DfID) to strengthen the infrastructures of fragile countries and increase stability there. Where do you want to spend the money, DfID, or 5 star hotels? You do the math.

3. Enable safe, legal routes for resettlement of genuine refugees. Would they even need a long stay in a processing centre on UK soil after dangerous water crossing, if you took safe, legal routes for resettlement more seriously? Take as example the priority given to Ukraine refugees, and how abysmal this home office under this government was at managing Ukrainian processing - sending them here and there, where no one was there to help them. And that’s what we call our gold star fast Lane process. Despite Tories paying lip service to liking safe, legal routes, the number of people resettled under the government’s UK resettlement scheme was 1,171 in the 12 months to September 2021, down by about 45% year on year.

4. This is the idea I like best. Process UK humanitarian visas on French soil, and bring them across on ferries. Genuine asylum seekers in northern France hoping to reach the UK to claim asylum, so happy to place themselves into the hands of our home office, could register their claim with UK officials and then be placed on ferries to be brought to the UK while their claim is processed. You want the Rwanda scheme because you are led to believe it hurts the business model of the people smugglers? The simple MoonRabbits Ferry to Freedom Solution utterly smashes through the business model of the people smugglers does it not?

I shall enjoy your grovelling apology - as I'm sure you're an honest and honourable individual - when I'm eventually vindicated.

More likely of course, that you try and wiggle out if it, and say that was always going to happen anyway, and not what you really meant or ever meant, and you were right (at all times) all along but I'll trust in your world-leading integrity 👍

But bad times are coming.

Those who don't understand this are probably Liberati who don't get it.

2. The evidence shows that increasing levels of wealth in developing countries leads to more economic migration away from them, not less, as smartphones and the internet open up new possibilities. Stability would be nice, but it's not within our gift. We'll do whatever the US decides; if that includes bombing AN other Middle Eastern country, that's what will happen. And it's maths.

3. Safe, legal routes, YES, but the application, processing, and validation of the asylum claim must be done in situ before they get on that safe legal route. Otherwise it's just inviting a stampede.

4. We want the people traffickers to stop because we want the people to stop. Your solution is like saying we should get the police to stab everyone on sight because it would put all the criminal stabbers out of business. It would, but all it would do is replace freelancers with a taxpayer funded service. What on earth would be the point.

But get beyond that and you’re reminded he was Boris’s right hand man, presided over much of the mess and has no vision. We’re in for a bleak couple of years.

What's he got to look forwards to? A completely over-spend system, a public that thinks more spending is good, and (Apart from Reeves) no help whatsoever.

Weight it according to expenses as a proportion of expenditure for median or average households is the sensible solution, as opposed to homeowner households as is currently done. Indeed given that inflation is a sharper problem for those who have to pay housing as well as every other cost as opposed to those on the same income who live cost-free for housing, weighting it according to non-owners would make more sense than owners, but average is surely the only accurate choice?

Housing and energy is the highest expense for the average household, forming on OBR statistics 28-33% of household budgets. So it should be weighted 28-33% accordingly, instead home owner based CPI weights it combined to a meagre14%.

Telling households that inflation is low because housing, electricity, gas and water combined are only 14% of CPI when they actually account for 28-33% is false and misleading data.

I like to play me Hans Zimmer.

It kept a roof above my head and the wind and rain away which is its purpose and why it is the most expensive item in my budget.

Because they know that if they can't get to Britain then those that come to France - and loiter there indefinitely in high numbers - would drop drastically.

Are you such a Libtarded Liberati that you can’t perceive the truth?

How much do people reckon Roe vs Wade is going to have an impact coming up?

Especially amongst young who are more politically motivated but generally underrepresented in polling due to normally lower turn outs.

Could the Dems hold onto more seats than expected as a result?

Georgia Senate - three polls out today (all fieldwork up to yesterday)

Survey USA - Warnock (D) +6

Echelon - Walker (R) +4

Remington - Walker (R) +4

But note Survey USA is A rated pollster per 538. Remington is B rated, Echelon B/C.

Literally anything could happen!

If they "let" a boat sink there will be a steely purse-lipped chorus of "It was their choice to put to sea". Letting the migrants die will be seen as bravery. A single focus-grouped phrase in the mouth of the PM or home secretary or minister for the immigration crisis, shocking to the left, centre, and centre-right but balm for Alf Garnett and what used to be the "red" wall, and the Tories will have the election in the bag.

Do you really think immigration can climb to become a main issue, big enough to achieve NOM but not THE main issue, big enough for a win?

Momentum.

Bellyflop of the month, though, thinking Brown changed inflation target from RPI with housing in it to CPI without, and being told the previous measure was RPIX, without housing in it. That stopped him in his tracks for half an hour but now he has found that RPIX includes the vat element of ground rent or some such shit while CPI doesn't, so he was right all along. Nimby Brown out to do Bart down.

And what he wants is a Heath Robinson arrangement anyway: put hpi into the inflation figures so the bank will notice and do something about it, when its primary effect will be an insane feedback loop simply increasing inflation. Instead of just giving the bank a separate, primary duty to control house prices.

But we don't need anecdotal stories or data, we have actual real data. Housing cost as a proportion of household budgets is a known figure, that should be its weighting. Not spin it to what you or I want, but what is actual fact.

Housing costs are a known proportion of expenditure, and their change in price levels is also known. Don't try and spin it for certain cases, go with actual weighting that it really is. Which is double the CPI figure.

"This is an estate community and it is very close to the hotel.

"I don't want to be judgemental about the people coming in but we have had situations before because we are close-knit estate - and, if you are going to put people in a hotel near a close-knit estate, who knows what could happen?"

https://www.bbc.co.uk/news/uk-england-norfolk-63500045.amp

Congratulations-Mazel Tov to @netanyahu for the electoral success. Ready to strengthen our friendship and our bilateral relations, to better face our common challenges.

https://twitter.com/GiorgiaMeloni/status/1588239403717050368

Some might not have seen their prices rise on the average amount, some might have seen it go up by much more than average, but the average citizen has on average seen the average change, which is why averages exist.

If housing costs come down as a share of expenditure their weighting should fall accordingly, if it goes up, it should fall accordingly. But it shouldn't be weighted half the actual OBR figure because of some edge cases.

Second hand cars, or fridges, or washing machines, or plenty else can be bought, but we still have their prices in CPI based on what they cost and weighted based on expenditure. But CPI downweights housing because it excludes lots of housing costs and is based primarily on homeowner data instead of average data.

Include average data and the problem is resolved.

It may well be that Starmer/Cooper end up being perceived as being more likely to find pragmatic and, yes, tough solutions that could actually work, without having to resort to the fatuous dog whistles of the Tories and their fellow Faragist travellers. People are paying very little attention to the plan that Cooper has proposed.

It may seem petty to you, but I'm sure the millions of people struggling to pay their rent or save a deposit as prices have risen and risen and risen its anything but petty.

If average figures were used, then using edge cases to argue against it would be silly. But they're not. The OBR says housing and energy are literally over double what CPI weights them at.

It's Brexit in reverse: the EU becomes much more hardline on immigration and asylum, stopping anyone coming in, and the Brits vote "in" to override the innane brain dead Wokery of their own established parties of government who import this reflexive crap across the anglosphere from America.

Also this issue will pale into non existence as winter exacerbates the NHS crisis and stops the boats crossing.

It's now 55/45 wrt the Senate election.

https://projects.fivethirtyeight.com/2022-election-forecast/senate/

They are all discussing house prices - homeowners will be greatly displeased by the likely impending crash, and while some people will be eagerly awaiting a dip, those aren't likely to be Conservative voters who, by and large, are already old and own their own properties. Boat people are a distant worry when the value of your main asset plummets 20% and the cost of your mortgage rises by several hundred pounds a month.

Fwiw, they are also seriously discussing the likelihood of rolling blackouts this winter. If that happens, plus a series of public sector strikes, the "winter of discontent" narrative is going to kill off any Sunak bounce and Lab majority nailed on in two years.

There was a French slogan when Chirac was up against Le Pen, 'Vote for the crook, not the Fascist.'

In Israel they've voted back in a man who is both a crook *and* a Fascist.

So we left, and the Tories we able to do CRAZY SHIT, and we all got royally screwed.

So yes, a campaign of "Stop these stupid fuckers being able to do it again" has a decent chance of success.

Before Brexit we could vote Dan Hannan out of office.

Now we are stuck with him for life, but maybe we could neuter him...

https://actuaries.blog.gov.uk/2021/08/23/measures-of-price-inflation-rpi-cpi-and-cpih/

ansd as a bonus explains why the difference between CPI, CPIH and RPI is not part of the great anti-Bart conspiracy.

https://www.gridwatch.templar.co.uk

Edit - and that figure is worse than it looks, because yesterday we were exporting power, today we're importing it.

*stares off into distance

Including HPI within inflation, weighted properly to what housing actually costs households, as happened until RPIX was dumped wouldn't be an insane feedback loop. Including MIPs instead of HPI would create a feedback loop which is why it very sensibly wasn't included in RPIX which I agree with. HPI and rent etc should take the full share of housing costs proportionately weighted to the average household budget not rate-sensitive MIPs.

1. It distracts from how they've managed to wreck the economy.

2. It distracts from how they've managed to wreck public services.

3. Lots of lefties - including myself - won't be able to help ourselves and will want to talk more about our compassion for refugees than about fixing the perceived problem.

Will it make enough of a difference to swing the election and prevent defeat, or will it only make a marginal difference and save a handful of seats? I don't honestly know, but it's a test for Labour and flunking it will have consequences.

But I admire your compacency.

https://www.bbc.co.uk/iplayer/episode/m001dslq/bbc-news-at-six-03112022

"2007, but Gordon Brown changed inflation from RPI which includes housing to the discredited CPI which does not, and Tory Chancellors have kept that change as it fraudulently pretended inflation had gone away."

Has anyone ever been more bang to rights?

https://www.windy.com/?50.575,-4.196,5,m:ffWafCz

Dev n Corn seem to have cornered the market in wind.

RPIX excludes the MIP to avoid the feedback loop problem which is entirely sensible, but it still includes housing with housing depreciation etc in a way that CPI doesn't.

If you think housing = MIP alone you couldn't be more wrong.

Whatever the scale, it's being counter-balanced (and perhaps more) by impact of rising cost of living, which is also affecting younger voters, esp. young families.

Can we have a nice chat about how Cambridge is really part of the North instead?

Your problem is that you don't understand that HPI is a conceptually different thing from CPI or RPI. No matter how house prices balloon there is a limit to what people can afford to spend to house themselves, what with needing to eat stuff and fuel their cars etc. and not being on unlimited wages. So there is NO proxy for HPI which you can plug into the other indices which will make the BoE say Lawks, CPI is running at 500% all of a sudden, we must crash the market to get back on target. It doesn't happen because it just doesn't work that way, not because of skulduggery by Brown or Osborne or anyone else.

And those who are in this financial position are by no means all Tory voters or all aged 50+.

Personally I would love a house price crash and house prices absolutely to break the floor (it's about time!), but tbf most of my neighbours probably have an attitude similar to your friends'.

Although it somehow forgets to mention the University of Cambridge is also based there.

Will be the capital of course of the restored Kingdom of the Wuffingas

"Don't want to be judgemental" - lol.

How fitting that "close-knit" rhymes with "full of sh*t".

Absolutely classic xenophobia.

I'm not sure what kind of estate that person is talking about, but I've lived on council estates and also estates of privately-owned houses and none of them have been particularly close-knit. Perhaps about two generations ago they may have been.

There is a limit to what people can afford to spend to house themselves, which is why I didn't propose replacing CPI with HPI, but rather weighting it properly, but it is not just a part of household expenditure but on average the biggest part of household expenditure which is why it should be there and properly weighted. Are you familiar with the concept of weighting and understand what it means?

If housing and energy make up 28% of household expenditure, it should be weighted to 28% within CPI, not down-weighted to half that. If for some reason housing and energy proportionately cost less in an era of high-inflation, then the weightings should adapt and adjust accordingly. Unfortunately since CPI for no good reason excluded housing inflation and downweights housing and energy to half its real weighting, that makes CPI data completely flawed.

But how about you say what it should be instead? If housing and energy are 28% of expenditure on average, then should housing and energy in your eyes be weighted to

A: 14%

B: 28%